- EquityResearch

- Posts

- The Barbell Portfolio: Built for Chaos, Designed for Growth

The Barbell Portfolio: Built for Chaos, Designed for Growth

This Investment Strategy Feels Illegal (But It’s Not)

Anshulika Bansal

May 13, 2025

Hey friend,

You want to make money… but also not lose it all in a market crash?

Yep, same here.

If you’ve ever felt torn between going all in on high-growth tech stocks or hiding in the safety of government bonds like a financially anxious squirrel…you’re not alone.

The truth is, investing feels a lot like adulting:

You want to take bold steps, but you also don’t want to end up crying over your portfolio on a Monday morning.

Enter the Barbell Strategy - a smart, balanced approach to investing that lets you be both bold and boring at the same time. Yes, it’s a thing.

Let’s break it down.

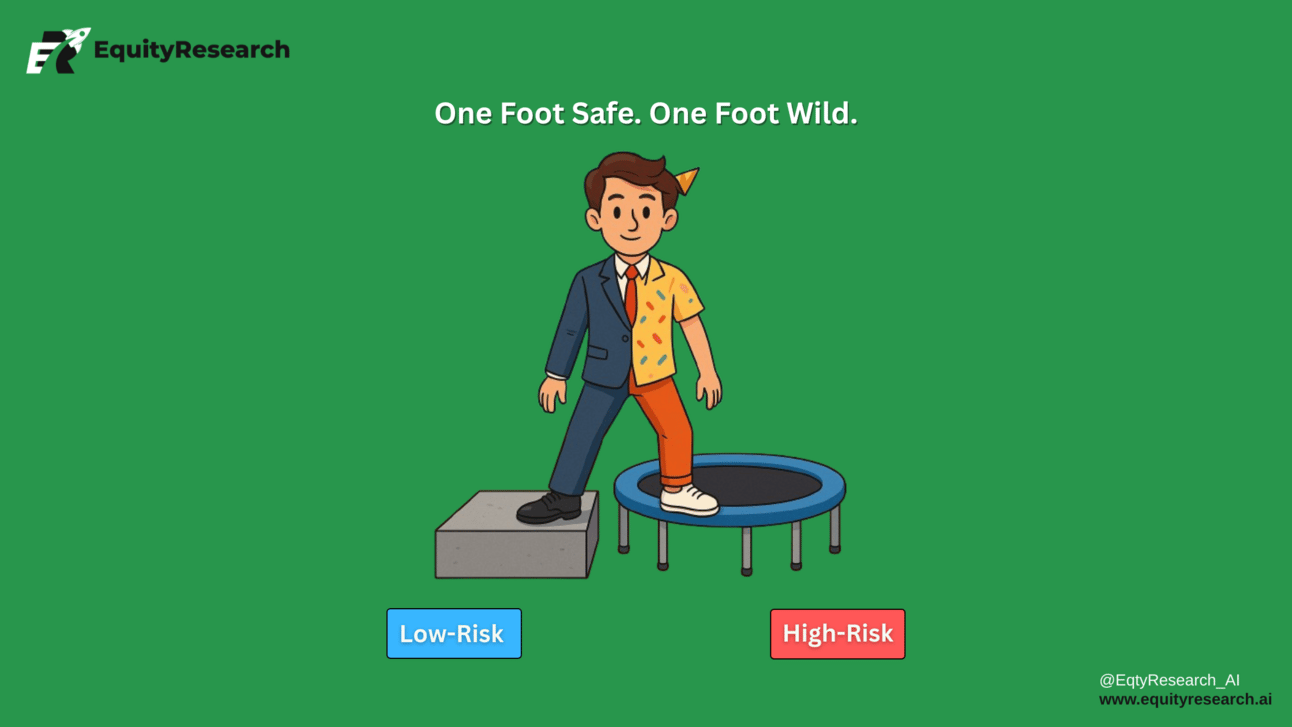

Safe When You Need It. Wild When You Want It.

What Is the Barbell Strategy?

Imagine a barbell at the gym:

Big weights on each side, and nothing in the middle.

Your portfolio does the same:

● One side = Low-risk, safe stuff like cash or short-term bonds (the cushion).

● Other side = High-risk, high-reward assets like growth stocks, or that edgy AI startup your cousin’s friend is launching.

The middle—aka “medium risk” stuff—is left out. Why?

Because the middle gives you mediocre returns without the safety of the low end or the growth potential of the high end. Meh.

Why is this strategy smart?

Because you’re:

● Protecting your wealth with boring-but-safe stuff

● Taking shots at serious upside with a small slice of your portfolio

● Avoiding the mushy, unpredictable middle

In plain English: You’re not going broke, but you still get a shot at getting rich.

Think of it like this:

My left foot is on solid ground. My right foot is on a trampoline.

That’s the barbell strategy.

The investors with the BEST returns aren't the ones with the most complex strategies. They're the ones who simply stuck around the longest.

How to build your Barbell Portfolio?

So, you’re sold on the idea—play it safe with most of your money, take bold bets with a small slice.

But how do you actually put this into action without feeling like you’re blindly throwing darts at a financial dartboard?

Here’s how to build your barbell portfolio step-by-step (no spreadsheet obsession required):

Figure Out Your Risk Tolerance

How much risk can you actually stomach?

Define Your “Safe” and “Risky”:

· Safe could be T-bills, ultra-short bond ETFs, or money-market funds—whatever you trust to preserve principal.

· Risky might be biotech small caps, crypto tokens, or deep-out-of-the-money options—just make sure you’re OK with a 100% loss on that slice.

The key here is to be honest. If a 20% dip makes you cry into your cereal, you’ll want to lean safer.

Know your “why” before you start buying. Otherwise you’re just guessing…

Stack the Safe Side

Put 70–90% of your money in low-risk stuff:

· Cash

· Short-term bonds

· High-yield savings

This is your safety net. It doesn’t grow fast—but it keeps you sane.

Add Some Spice on the Risky End

Use 10–30% for bold bets:

· Emerging market stocks

· Startups

· Crypto

Small slice. Big upside. Controlled chaos.

Rebalance Once in a While

Markets shift. Your allocations will too.

Check in, adjust, and keep that barbell balanced.

(Just like at the gym—but without the sweat.)

As your risky bets either soar or crash, rebalance back to your target split—this locks in gains and enforces discipline…

If you want to pick quality stocks for your barbell portfolio,

go to EquityResearch and input the ticker.

Here’s a simple framework to get started

Framework #1: Conservative Setup

● 90% in cash, short-term bonds, or fixed-income funds

● 10% in moonshot stocks or volatile assets

Framework #2: Moderate Setup

● 80% low-risk

● 20% high-risk

Framework #3: Aggressive Setup

● 70% safe stuff

● 30% spicy growth bets

Pick your flavor based on your risk appetite.

If seeing red on your dashboard makes you sweat, start conservative.

If you secretly enjoy chaos, well... you know what to do.

PRO TIP: By shifting from 90/10 → 80/20 → 70/30, you’re simply choosing a point on the risk spectrum that matches your time horizon and stomach for volatility.

Real-Life Example

Let’s say you’ve got $10,000:

● $8 000–$9000 go into government bonds, debt funds, fixed deposits, or even a high-interest savings account.

● $1000–$2000 go into that edgy fintech stock, small-cap mutual fund, or a basket of handpicked AI startups.

If the risky stuff crashes…you still have 80–90% safe.

If it flies…Wow! You look like a genius.

The Best of Both Worlds: Safety + Upside

Why choose between protecting your money and growing it when you can do both?

The beauty of the barbell strategy is that it doesn't force you to pick a side—it lets you invest like a realist and dream like an optimist.

Here’s why it works so well:

It Manages Risk Like a Pro

You keep most of your money safe, tucked away in low-risk assets.

But… you still leave room for some bold, high-upside moves.

It’s like having an umbrella and sunglasses—you’re ready either way.

It’s Refreshingly Simple

No complicated spreadsheets.

No ten-step rebalancing rituals.

Just two sides: safe and spicy. You’re done.

It’s Super Flexible

Whether you’re ultra-cautious or low-key chaotic, this strategy adapts.

You control how much risk you take—not the market.

It Thrives in Chaos

Market crashing? You’ve got safety.

Market booming? You’ve got growth.

Basically, this strategy is like that one friend who always stays calm during group drama.

Bottom line: It’s a strategy for people who want to grow their wealth without losing their minds.

Final Thoughts: Offense + Defense = Long-Term Success

The Barbell Strategy is basically the financial version of "Work hard, party harder."

Except here it’s "Be safe, invest smartly risky."

It’s not about timing the market.

It’s about preparing for both sunshine and storms.

If you want to pick quality stocks for your barbell portfolio,

go to EquityResearch and input the ticker.

Disclaimer: This newsletter is for informational purposes only and should not be considered financial advice. Always consult with a financial advisor before making investment decisions.